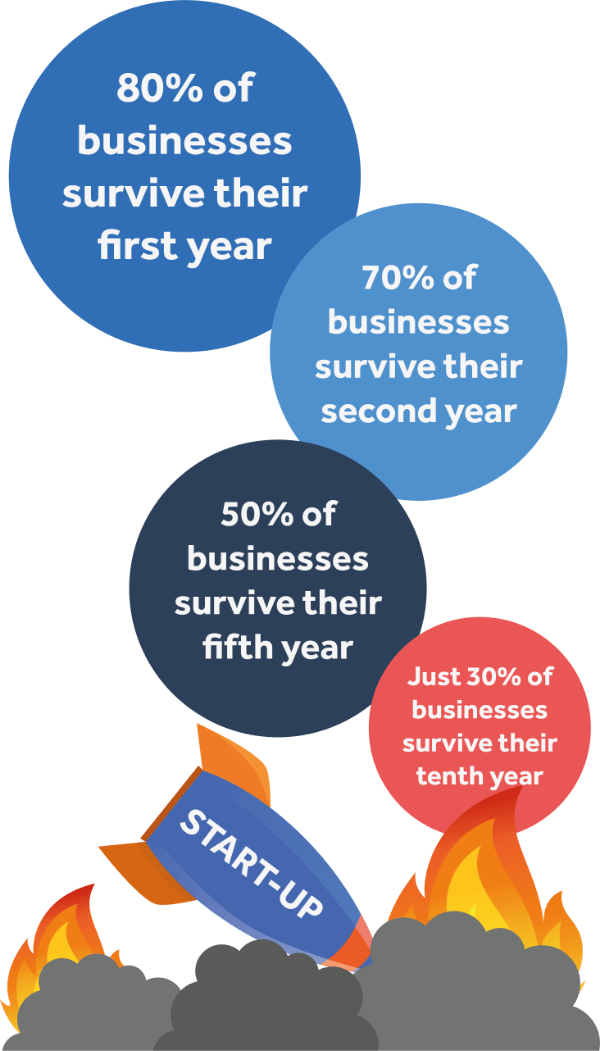

Why Liability Matters for Small Businesses

Small business ownership carries a host of daily challenges, but few are as critical or as often overlooked as managing liability risk. From the very first client interaction or sale, there’s the potential for unexpected accidents or disputes. Whether it’s a customer slipping on a wet floor or a delivery gone wrong, incidents can happen within moments and often spiral into significant financial exposure. According to a survey featured by the U.S. Small Business Administration, over half of small businesses have faced legal action from customers, vendors, or even competitors. The cost, both financially and emotionally, can derail a business just as it’s beginning to grow.

Many entrepreneurs, especially those just starting out, might be tempted to put off thinking about liability insurance until “later.” However, delaying this decision can put the entire business at risk. Even something as minor as a social media error or a simple misunderstanding with a client has the potential to turn into a costly legal affair. That is why it is smart to learn more about general liability insurance as soon as operations begin. Having a foundational level of protection against the unexpected empowers business owners to make decisions confidently, knowing they have a safety net in place.

Common Risk Factors That Lead to Claims

While each small business is unique, several common risk factors tend to trigger liability claims. Recognizing them is the first step in mitigating their potential impact. One of the most frequent risks is accidents on business premises, such as slips, trips, and falls. Even a well-lit, well-maintained space can become hazardous with wet floors, uneven surfaces, or clutter. The consequences can be both financial and reputational, especially if injuries are severe.

- Slips and Falls: These incidents are the most common starters of lawsuits and insurance claims for small business owners. Even a single loose tile or freshly mopped floor can result in expensive medical bills or settlements.

- Property Damage: Accidental damage to customer property—think dropping a client’s phone or scratching a parked car—can create unexpected liabilities and claims, even for businesses with the best of intentions.

- Product Issues: Defective or improperly used products can land a business in hot water. Even companies with excellent safety track records can face lawsuits if customers suffer harm because of products or services.

- Reputational Harm: Missteps in advertising, such as copyright infringement or making exaggerated claims, are increasingly risky in today’s digital era. Digital content moves fast, making errors or oversights more common—and often costlier.

- Completed Operations: Providing a service doesn’t end the risk when the job is done. If a past service causes injury or financial loss after it’s completed, responsibility can loop back to the service provider unexpectedly.

The complexity of these risks means business owners can never entirely predict where the next claim might arise. In many cases, it’s a simple error or oversight, rather than negligence, that sparks lengthy legal proceedings or insurance claims.

How Liability Insurance Protects Owners

General liability insurance acts as an essential safety net for companies of all sizes. The threat of lawsuits is a reality for any business, and when legal action occurs, costs escalate quickly. Legal defense fees, court costs, settlements, and even small claims can drain bank accounts or disrupt daily operations. Without financial support, these expenses can leave owners facing debt or threaten the future of the business itself.

Liability insurance typically covers a range of scenarios:

- Attorney and court costs when defending against lawsuits

- Medical expenses for injuries occurring on company property

- Property damage repairs or replacement due to business activities

- Settlement payments for lawsuits involving advertising errors, such as libel or slander

Having this protection means owners aren’t left to grapple alone with the financial fallout from an accident or legal challenge. Many commercial landlords, lenders, and even customers require evidence of insurance before moving forward with a contract or partnership. By ensuring that this coverage is in place, businesses project professionalism and trustworthiness, essential qualities for long-term success.

Practical Tips to Reduce Liability Risks

Proactive risk management is one of the most valuable habits a business owner can develop. By identifying and addressing liabilities before they turn into claims, companies can not only protect their finances but also foster trust and reliability. Here are five practical steps to reduce day-to-day risks:

- Walk through your premises regularly. Look for spills, debris, frayed carpeting, or other hazards, and correct issues immediately. Clear pathways and well-maintained spaces minimize risk.

- Invest in training for all staff, including part-timers or seasonal workers. Basic safety knowledge and proper customer interaction protocols help prevent misunderstandings or accidents before they occur.

- Put every business agreement in writing. Clearly outline responsibilities, deliverables, and expectations. Having contracts and service agreements ensures all parties understand the rules and lessens the chance of disputes.

- Develop a habit of documenting everything. Keep logs of customer complaints, safety measures, employee training, and repairs. Well-kept records can be invaluable in the event of a liability claim.

- Review your insurance coverage annually, or after any major business change. Growing staff, new equipment, or added services can all impact liability risk, so make regular policy reviews part of your yearly checklist.

By weaving risk-reduction practices into the daily routine, businesses not only lower their odds of lawsuits but may also see savings through lower insurance premiums over time.

Trends in Liability Claims and What They Mean

The landscape of small business risks is constantly evolving—and so are the kinds of liability claims being filed. Recent years have seen an uptick in claims linked to digital marketing, data handling, and consumer privacy rights. As businesses embrace new technology and more online interaction, the likelihood of facing legal action over privacy or intellectual property is on the rise. The rise in general liability claims highlighted by industry news serves as a timely reminder that risk is always shifting.

Consumer awareness is also up—people are more likely to advocate for their rights and pursue claims when they believe services or products have fallen short. The growth of e-commerce has brought new exposures around customer data, website terms, and online reviews. Staying informed and periodically updating processes and policies can help business owners prepare for, and ideally avoid, the challenges posed by new trends.

Key Resources for Small Business Owners

Navigating liability exposures doesn’t mean going it alone. A wealth of resources is available to help small business owners stay informed, organized, and prepared. For example, the Small Business Administration website offers free guides and planning toolkits designed for emergency preparedness and risk management. Such resources are an excellent starting point for learning about legal compliance, safety requirements, and smart operational practices.

Joining local business groups or industry associations also provides the benefit of shared experience. Peers can offer firsthand accounts of risk management strategies that work—and sometimes, those that don’t. Additionally, connecting with trusted insurance professionals ensures coverage remains suited to your evolving needs. Building a network of support and knowledge can transform daunting challenges into manageable problems, giving business owners the confidence to thrive and grow in any environment.